TL;DR: A Letter of Protection lets Florida accident victims get medical care now and pay later from the settlement, after PIP runs out and bills pile up.

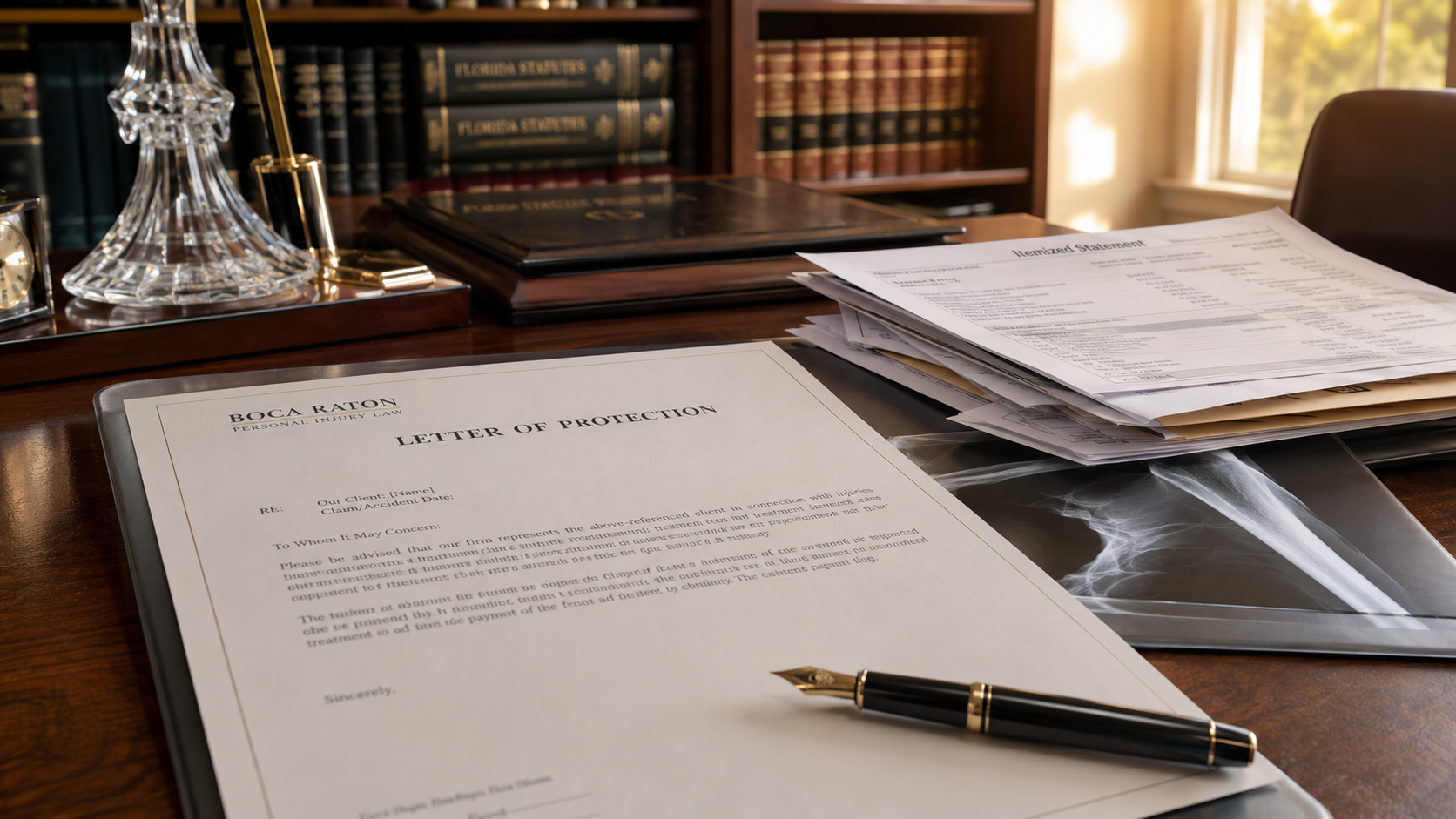

A Letter of Protection is a written promise from your personal injury attorney to a medical provider that the provider will be paid out of any settlement or verdict in your accident case, in exchange for treating you now without billing your health insurance or sending the bills to collections. In Florida, where the no-fault Personal Injury Protection cap of $10,000 is exhausted faster than most people expect after a serious crash, Letters of Protection are often the difference between getting the orthopedic surgery, MRI, or physical therapy your doctor is recommending and waiting months while the bills go unpaid.

Why Florida Accident Victims End Up Needing a Letter of Protection

Florida’s no-fault auto insurance system gives every covered driver $10,000 in PIP benefits to cover the first wave of medical bills after a crash, regardless of who caused the accident. That sounds like a lot until you look at what serious treatment actually costs. A single ambulance ride and emergency room visit in Boca Raton can run $4,000 to $7,000. An MRI is another $1,200 to $2,500. A surgical consultation, follow-up imaging, and a few weeks of physical therapy can blow through the remaining PIP balance before the swelling has even gone down.

What happens next is where most clients get blindsided. Health insurance may pay part of the ongoing care, but it will almost always assert a lien against any eventual settlement, taking back what it paid. Some providers will not accept health insurance for accident-related care at all because they expect higher recovery from a personal injury settlement. Others will treat the patient but send the bills to collections within 90 days. A Letter of Protection short-circuits all of that.

How a Letter of Protection Actually Works

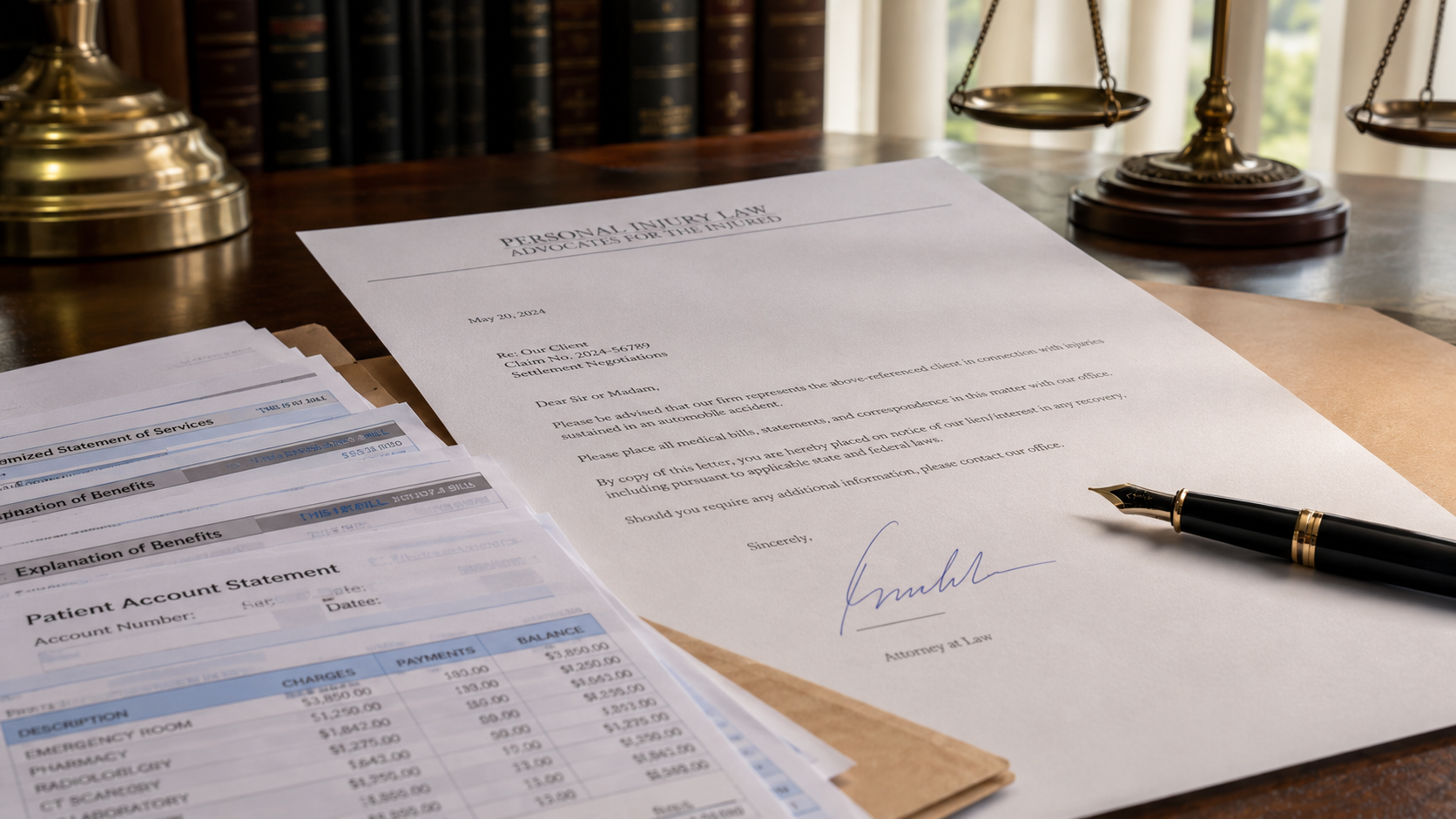

Your attorney signs and sends a Letter of Protection on firm letterhead to the medical provider. The letter typically promises three things: that your attorney represents you in the personal injury matter, that the provider’s bill will be paid from the proceeds of any settlement or judgment before funds are distributed to you, and that the provider agrees to hold off on collections while the case is pending. The provider continues to treat you. The bills accumulate but do not damage your credit. When the case resolves, your attorney’s office distributes settlement funds in a defined order, with the LOP providers paid out of the gross recovery.

What the LOP Is Not

A Letter of Protection is not a guarantee of payment regardless of case outcome. If the case is lost or recovers nothing, the underlying medical debt typically remains yours, though many providers will negotiate that final balance significantly. It also is not a substitute for health insurance for unrelated medical care. The LOP only covers treatment related to the accident injuries.

The Florida Providers Who Routinely Accept Letters of Protection

South Florida has a deep ecosystem of providers who accept LOPs because they understand personal injury litigation and know the system. Orthopedic surgeons, neurologists, pain management physicians, chiropractors, physical therapists, and diagnostic imaging centers in Boca Raton, Delray Beach, Fort Lauderdale, and West Palm Beach commonly work on LOP arrangements with established personal injury firms. The relationships matter. A provider that has worked with our firm across many cases knows the firm honors its LOPs, and that history is what gives clients access to specialists they might otherwise be turned away from.

For clients without health insurance, or with health plans that have $5,000 deductibles, an LOP is often the only viable path to the imaging and surgery their case needs to prove damages. For clients with health insurance, an LOP can still be the smart choice because it avoids the health-insurance subrogation lien that would otherwise eat into the eventual recovery.

How an LOP Affects the Final Settlement

Settlement distribution in a Florida personal injury case follows a defined order. After the gross settlement is reached, attorney fees and case costs come out first under the contingency agreement. Then come the LOP providers, the health insurance liens (if any), and any other valid claims against the recovery. Whatever remains is the client’s net payout.

This is why the conversation about an LOP needs to happen with eyes open. A $50,000 settlement on a case with $20,000 in LOP medical bills, $5,000 in case costs, and a one-third contingency fee leaves about $8,300 for the client, before any health insurance subrogation lien. The math changes dramatically with larger settlements, larger medical bills, and successful negotiation of provider balances at the end of the case.

The negotiation step matters. Experienced attorneys often negotiate LOP balances down significantly at settlement time, especially when the recovery is less than expected or when the provider’s billed rate is higher than the typical insurance-negotiated rate. A skilled lien resolution conversation can shift thousands of dollars from the provider’s share to the client’s pocket.

When Florida Law Limits or Complicates Letters of Protection

Florida’s collateral source rule and recent tort reform changes have affected how LOP bills are presented at trial. Defense attorneys frequently argue that LOP-billed amounts are inflated above what insurance would have paid for the same services, and Florida courts have ruled in various ways on whether the full LOP amount, the amount actually paid, or some median figure should be presented to the jury. The Florida statute governing motor vehicle insurance and reimbursement is publicly available at Section 627.736, Florida Statutes, and it is the foundation for understanding how PIP exhausts and where LOPs enter the picture.

What this means in practice is that an LOP arrangement should always be paired with thorough billing documentation, expert testimony when needed about the reasonable value of the services rendered, and a clear-eyed settlement strategy that accounts for the negotiation power on both sides. The cases where LOPs work best are cases where the medical care was clearly necessary, well-documented, and supported by treating physicians willing to testify about the reasonableness of the care.

What to Do If You Are Hitting the PIP Cap

If you are within the first few weeks after a Florida car accident and you can see your PIP balance shrinking faster than your recovery, the time to call a personal injury attorney is now, not later. The earlier in treatment the LOP relationships are established, the cleaner the case file becomes. Providers prefer to start working under an LOP from the beginning rather than convert mid-treatment, and the documentation is stronger when the attorney is involved early.

Practical steps to take immediately include keeping every Explanation of Benefits document from your PIP carrier, noting the date PIP exhausted (or projected to exhaust), making a list of every provider currently treating you, and gathering the contact information for any specialists your treating physician is referring you to. When you sit down with a Boca Raton car accident attorney, those documents shape the LOP strategy for the case.

For Boca Raton, Delray Beach, and West Palm Beach residents who have just been in a crash, the most important call to make is one that gets the LOP infrastructure set up early. Schedule a free consultation with our firm to walk through what your PIP coverage looks like, where the gaps will be, and which providers will accept an LOP for your specific injuries.

Frequently Asked Questions

What is a Letter of Protection in a Florida personal injury case?

A Letter of Protection is a written agreement from your personal injury attorney to a medical provider promising payment from any settlement or verdict in exchange for treating you now without billing health insurance or sending bills to collections. It is most often used after Florida’s $10,000 PIP cap is exhausted.

How fast does PIP usually run out in a Florida car accident case?

PIP can exhaust in days to weeks for moderate to serious injuries. An ER visit, ambulance ride, and one MRI often total $7,000 to $10,000 by themselves. For accident victims who need surgery, specialist consults, or extended physical therapy, the $10,000 PIP cap is reached before treatment is even half finished.

Will I owe the LOP medical bills if my Florida injury case is lost?

Generally yes, the underlying medical debt remains your responsibility if the case recovers nothing. However, many providers negotiate balances significantly in losing or low-recovery cases. Your attorney should explain this scenario clearly before any LOP is signed so you understand the exposure.

Can I use my health insurance and a Letter of Protection at the same time?

Sometimes, but it depends on the provider and the health plan. Many health plans assert subrogation liens against personal injury settlements, which can complicate the math. Some providers prefer LOP-only billing for accident-related care. Your attorney will assess the right approach case by case.

What types of South Florida medical providers commonly accept LOPs?

Orthopedic surgeons, neurologists, pain management physicians, chiropractors, physical therapists, and diagnostic imaging centers in Boca Raton, Delray Beach, Fort Lauderdale, and West Palm Beach routinely accept Letters of Protection from established personal injury firms. The provider network varies by injury type and specialty.

How does an LOP change my final settlement amount?

Settlement proceeds are distributed in a defined order: attorney fees and costs, then LOP providers, then health insurance liens, then the client. Larger settlements absorb LOP balances more easily; smaller settlements can leave little for the client unless provider balances are negotiated down at the end.