TL;DR: Recovering lost wages after a Florida car accident takes documented proof: pay stubs, employer letters, tax returns, and medical work restrictions tied to the crash.

Recovering lost wages after a Florida car accident is a documentation problem first and a legal problem second. Insurance adjusters and defense attorneys will rarely accept a verbal claim that you missed two weeks of work, lost a $5,000 commission, or could no longer perform the side-gig income your household relied on. They want to see the records, and they want those records to connect cleanly to your medical work restrictions, your treating physician’s notes, and the way your earnings actually flowed before and after the crash. The clients who recover the most for lost wages are the ones who build that documentation file from the first week after the accident.

What Counts as Lost Wages in a Florida Personal Injury Case

Lost wages in Florida personal injury claims include every category of earnings you would have made but for the crash and your injuries. That covers regular hourly or salaried pay, overtime that you reasonably would have worked, commissions and bonuses you would have earned, tips, sick days and paid time off you had to use because of the accident, vacation time spent recovering instead of vacationing, and self-employment income lost while you could not work. It also covers loss of earning capacity, which is the projected reduction in your future ability to earn income because of permanent injury or restriction.

The breadth of categories is important because most accident victims initially think of lost wages as just “the paychecks I missed.” That narrow framing leaves real money on the table. A Boca Raton software engineer who missed three weeks of regular pay but also lost a quarter-end bonus opportunity has two distinct claim components. A Delray Beach restaurant server who missed shifts has both base pay and a calculable lost-tip figure. The Florida Statutes that govern damages allow recovery for all reasonably documented economic loss, and the cases that produce the largest results are the ones that document each category cleanly.

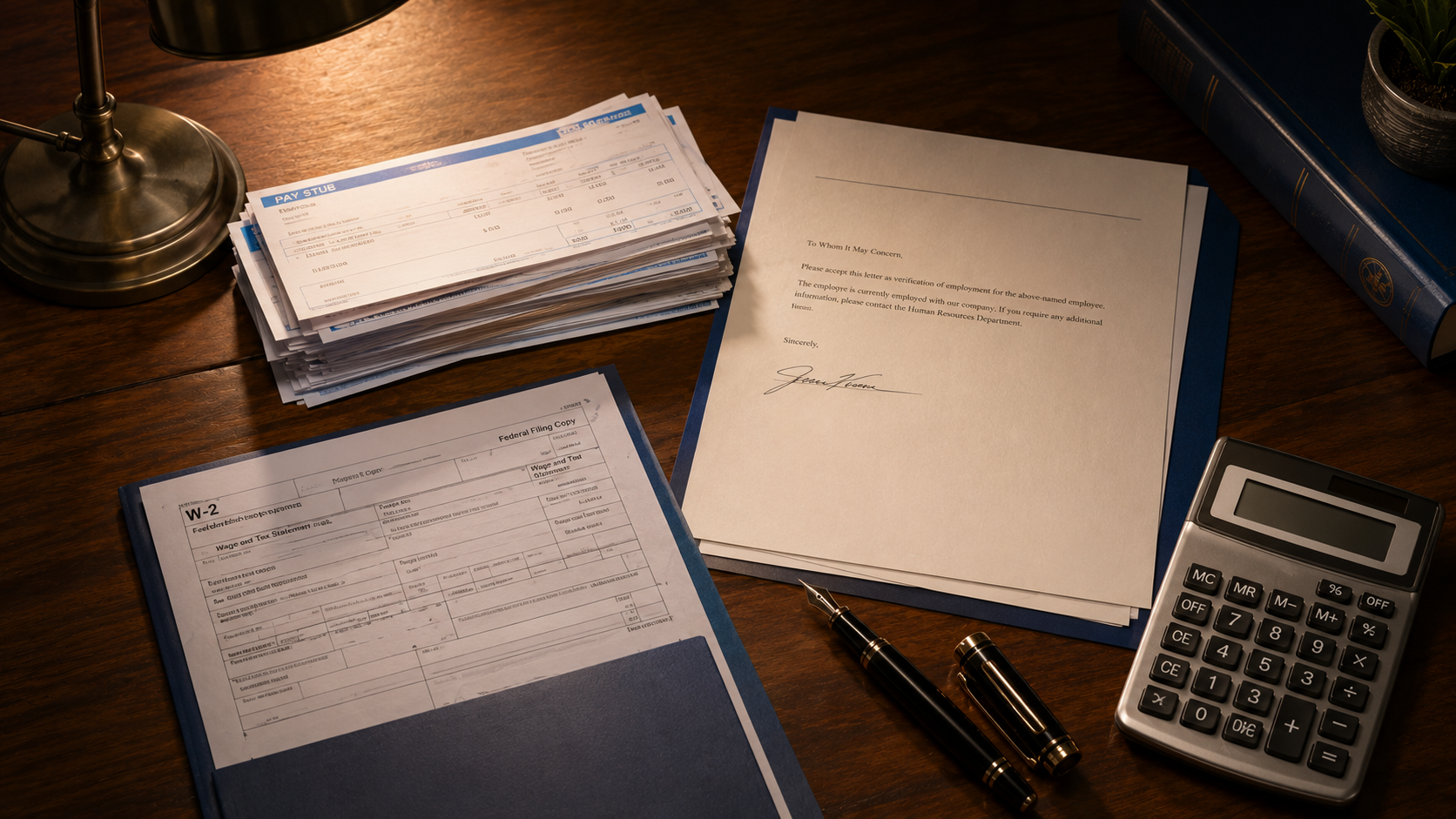

The Documents That Actually Win Lost-Wages Claims

For W-2 Employees

The foundation document is a wage verification letter from your employer, signed by HR or by an owner-level signatory, on company letterhead, that states your job title, your hourly rate or salary, your typical weekly hours, your typical overtime, and the dates you were unable to work because of the accident. The employer should also confirm any paid time off, sick leave, or vacation time you had to use, and indicate whether you returned to work in a reduced capacity. Pair the wage verification letter with twelve months of pay stubs from before the accident and every pay stub since. The before-and-after comparison is what defeats the insurance adjuster’s argument that you would not have earned that much anyway.

If you received any bonuses, commissions, or performance-based pay in the prior year, get documentation of those amounts as well. A copy of the bonus plan, the commission structure, prior years’ bonus payouts, and any communications about the bonus you missed all become evidence. A two-year W-2 history establishes your baseline earning capacity.

For 1099 and Self-Employed Workers

Self-employment lost-wages claims are harder, but they are often the highest-value claims because self-employed people often have more flexible time and higher per-hour rates than W-2 workers. The documentation here is more comprehensive. You need two to three years of personal and business tax returns including Schedule C, profit-and-loss statements covering the months before and after the accident, bank statements showing deposit patterns, contracts and invoices that document expected work you could not complete, and accounts receivable aging reports that show projects in the pipeline at the time of the crash.

For freelancers, contractors, and small-business owners across South Florida, a forensic accountant becomes valuable in mid-to-larger cases. The forensic accountant can build a defensible model of what you would have earned, what you actually earned, and the gap between the two. The cost of that expert is often more than recovered through the larger settlement that results.

The Medical Documentation That Ties It All Together

None of the wage documentation matters if the medical record does not establish that you could not work. Your treating physician’s notes need to specifically document work restrictions, how long they were in place, what activities you could not perform, and when restrictions were lifted. A return-to-work note that simply says “may return to regular duties” without explaining the prior restrictions weakens the case. A well-drafted note from an orthopedic surgeon or neurologist that explains why you could not lift more than ten pounds, sit for more than twenty minutes, or operate a vehicle for the first three weeks after surgery does the opposite.

This is one of the reasons we encourage clients to communicate openly with treating physicians about their job duties from the first visit. The physician needs to know whether you sit in front of a screen, climb scaffolding, drive long routes, or stand on your feet for ten-hour restaurant shifts. The restrictions in the medical record have to match the work you actually do.

How the NHTSA Cost Framework Affects Your Claim Value

Insurance adjusters and defense attorneys work with established frameworks for valuing crash-related economic loss. The National Highway Traffic Safety Administration’s research, summarized in NHTSA’s report that motor vehicle crashes cost America $340 billion in 2019, breaks crash costs into categories that include lost market productivity, lost household productivity, medical care, and quality-of-life impacts. The lost productivity component is significant and is the framework that informs how serious claims are valued at mediation and trial.

What that means in practice for your Florida case is that the wage documentation you build becomes a defensible numerical claim against an established benchmark. A claim that you lost $15,000 in income with no documentation is worth less than a claim that you lost $12,847 with pay stubs, an employer letter, and a corresponding medical work restriction. Numbers with proof move settlements; numbers without proof get discounted.

Future Lost Earnings and Loss of Earning Capacity

For more serious injuries, lost wages also include future earnings and loss of earning capacity. A Boca Raton or Fort Lauderdale resident whose permanent spinal injury means they can no longer do the construction work they had done for twenty years has a claim for the difference between their pre-accident career path and their post-accident earning trajectory. This is often the largest single component of damages in catastrophic-injury cases.

Proving future loss requires vocational experts, life care planners, and economists who can build defensible projections. The expert testimony quantifies the gap between the income trajectory you were on and the trajectory you are now limited to. Florida juries can and do award substantial sums for future loss when the documentation is rigorous.

What to Do Right Now to Preserve Your Lost-Wages Claim

Start documenting from the first day off work. Keep a calendar log of every day you missed, the reason, the medical appointments that day, and any restricted hours you worked. Request a wage verification letter from your employer in the first two weeks while the accident is still fresh in everyone’s mind. Save every pay stub, every direct deposit notification, every employer communication about your reduced schedule. For self-employed workers, save every email about a cancelled project, every invoice that was not sent, every contract that paused.

If you are reading this in the first month after your accident and you are losing income, the conversation to have now is with a personal injury attorney who handles these cases regularly. Our Boca Raton car accident attorneys work with clients across South Florida to build the wage-loss documentation file from day one. The earlier the file is built, the cleaner the eventual recovery. Schedule a free case review to walk through your specific employment situation and identify which documents you need to gather now.

Frequently Asked Questions

What kinds of income count as lost wages in a Florida injury claim?

Regular pay, overtime, commissions, tips, bonuses, sick leave and vacation time used because of the accident, self-employment income, and projected future earnings all count. The breadth surprises many clients who think only of missed paychecks. Florida law allows recovery for all reasonably documented economic loss caused by the crash.

How do I document lost wages if I am self-employed in Florida?

Self-employed claims require deeper documentation: two to three years of tax returns including Schedule C, profit-and-loss statements bracketing the accident date, bank statements showing deposit patterns, cancelled contracts, unsent invoices, and accounts receivable aging. A forensic accountant often becomes worth the cost in mid-to-larger cases.

What if my employer is slow to provide a wage verification letter?

Send a written request through HR with a deadline of seven business days. If the employer does not respond, your attorney can issue a formal request, subpoena records during litigation, or build the claim using your pay stubs and tax returns directly. Employer cooperation strengthens the claim but is not strictly required.

Can I still recover lost wages if I used sick days or PTO to cover the time off?

Yes. Florida courts have recognized that sick leave and paid time off have value, and using them for accident-related recovery is a real loss. The claim is for the value of the time you would have otherwise had available for other purposes, supported by your employer’s PTO accrual records.

How do work restrictions in my medical record affect the lost-wages claim?

Significantly. The medical record needs to establish that you could not perform your specific job duties, not just generic restrictions. Treating physician notes that document lifting limits, sitting tolerance, driving limitations, and standing endurance, tied to your actual job, are the bridge between your injury and your wage loss.

What about future lost earnings if my injury is permanent?

For permanent injuries that affect your ability to do your prior work, loss of earning capacity becomes a major claim component. Proving it requires vocational rehabilitation experts, life care planners, and forensic economists who can build defensible projections. These cases often produce the largest awards because future loss can extend decades into the future.